The Riksbank seems set to cut rates again

2024-25

I normally publish a longer post on Mondays and a shorter post on Wednesday. This week I planned to use the latter to comment on the outlook for Riksbank policy. But since it will announce the outcome of its policy meeting on Wednesday morning, I will publish the shorter post already today.

The Riksbank is in my view likely to cut interest rates again by of 0.25% and to signal further cuts in November and December. This will be the third cut, after the 0.25% cuts in May and in August.

There are several reasons for why the Riksbank will continue to ease monetary policy.

Inflation and economic activity

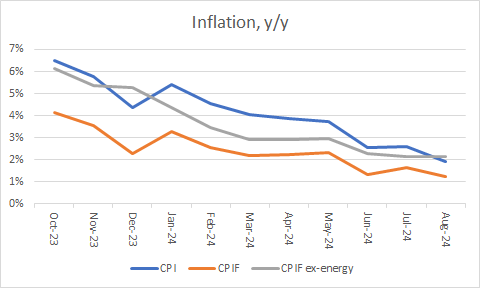

Most importantly, with year-over-year inflation measured by the CPI at 1.9%, CPI-F at 1.2% and CPI-FXE at 2.2%, Sweden has returned to price stability. Inflation has in recent months evolved much like the Riksbank expected and it appears likely that it will stay around target. That said, I believe that the balance of risks to inflation is to the downside.

Source: SCB

Sweden is experiencing a soft patch with rising unemployment. Plainly this is due to the dramatic tightening of monetary policy in Sweden and elsewhere.

Source: SCB

The weakness of the Swedish economy is readily apparent in teal GDP, which has grown little since 2021

Source: SCB

The external environment is worsening. The US economy is slowing, and price pressures are abating. In response, the Fed has started lowering interest rates, with the first step being a cut of 50 bps. The euro area, particularly Germany, is also experiencing a slowdown. But euro area inflation is stickier than US inflation and the ECB will therefore to be unable to add stimulus as quickly as the Federal Reserve. Economic growth among Sweden’s most important trading partners is therefore likely to be weak in the coming quarters. For a highly export dependent economy, that matters.

Policy expectations

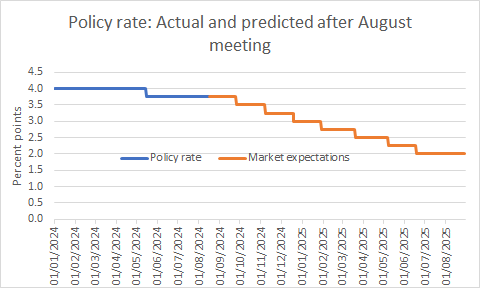

It is therefore not surprising that financial markets at the time of the Riksbank’s policy meeting in August priced in seven 0.25% cuts between then and the end of August 2025.

Source: my calculations on data from the Riksbank

A model-based forecast

Next, I update the forecasting equation for the Riksbank’s policy rate that I discussed in an earlier post. That model predicts a 0.29% cut in interest rates at this week’s meeting with a standard error of 0.15. Assuming normality, I can then compute the probability of a cut of 0.25% (which depends on the probability that change in the interest rate will fall in the range of ‑0.125% to -0.375%). I can use the same method to compute the probability of other policy choices.

The graph below shows the estimated probabilities. (Since this is the first time I use the model, it has no track record at all so they should be interpreted with caution). They key finding is that the probability of a 0.25% cut is almost 60%. However, given how well (or how poorly) the model has accounted for interest rate changes in the sample, there is almost a 30% probability of a 0.50% cut. The driving factor there is that the model uses CPI inflation, which was below 2% in August. I note that there is also some negligible probability of an even larger cut and of no cut or even an increase.

Source: my calculation on data from the Riksbank

Conclusion

Overall, with inflation at, or even below, the Riksbank’s 2% target, with the Swedish economy in recession and with the euro area and the US economies both weak, I expect a 0.25% cut this week.