Interest rate setting by the Riksbank 2021-24

2024-09

In this post I look at the interest rate setting behaviour of the Riksbank in the aftermath of the covid pandemic. I plan to return to the topic of Riksbank policy in the future and intend for the work presented here to serve as a starting point.

The analysis follows my earlier post on Interest rate setting by the SNB 2022-24 (published on 22 July). Thus, I can be brief. My back-of-the-envelope model of the change in the policy rate involves two explanatory variables: headline inflation and Riksbank’s policy rate. The model is thus extremely simple, as it necessarily will have to be, given the very limited number of data points.

Source: SCB and Riksbank.

Since the Riksbank employs flexible inflation targeting, one would expect some variable reflecting economic activity to enter the model to capture the trade-off between inflation and economic activity. However, despite some experimentation, that turned out not to be the case.

The likely explanation is that in this period policy was focussed squarely on bringing down inflation even at the cost of slowing growth. Indeed, one way to lower inflation could be to slow economic activity. If so, there is thus no trade-off to be captured. Is this true? Activity comes down, is that not the trade off?

I will start the analysis with the February 2021 policy meeting, that is a little more than one year before the first interest rate increase, which in the case of the Riksbank took place at the meeting in April 2022. The last observation is the June 2024 meeting.

Since the Riksbank had five policy meetings per year until the end of 2023, when it increased the number of meetings to eight, there are 19 observations in the sample. At 11 of these it changed the interest rate.

As in the cast of the SNB, I consider several explanatory variables:

A constant, which is related to the equilibrium real interest rate, r*, in the estimation period.

The change, if any, at the previous policy meetings. Central banks typically change interest rates several times in the same direction. This variable was highly significant in the case of the reaction function for the SNB in my earlier post.

The rate of inflation in the month before (to account for reporting lags) the policy meeting.

The level of the interest rate set at the last meeting.

The estimates (which I will not report in the interest of brevity) show that the decision made at the previous policy meeting was insignificant, that the parameter on inflation was positive and significant and that the parameter on the lagged interest rate was negative, significant, and about as large in absolute value as the parameter on inflation.

It thus appears that the Riksbank set interest rates depending on the difference between the interest rate and inflation, that is, the real interest rate. Re-estimating the model, the constant is -0.154 (t = 3.16) and the parameter on the real interest rate -0.089 (t = 9.25). The implied estimate of r* is therefore -1.7%, a little lower than -1% estimate for the SNB.

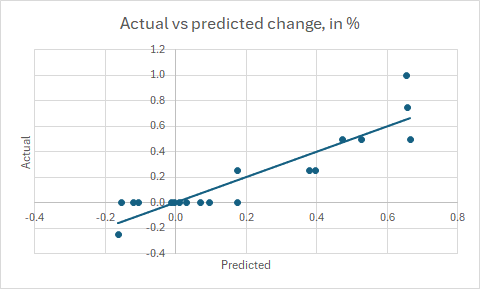

The scatter plot below shows actual versus predicted interest rate changes. As can be seen, the model appears to fit quite well, with a correlation of actual and fitted interest rate changes of 0.91.

Source: my estimates as described in the text.

The table below looks at the results for the 19 policy meetings in the sample. The first column shows the predicted interest rate change in percent, the second shows the same change rounded to the nearest 0.25% and the third column shows the actual change in interest rates in percent.

Source: my estimates as described in the text.

It is interesting to look at the results in some detail. In doing so, it should be kept in mind that while the analysis is conducted on the full data set, policy makers only had access to data on economic conditions up until the policy meeting.

The model is “wrong” (marked in red) on six occasions: in February, April and September 2022; February and June 2023; and June 2024. However, on these occasions the predicted change is close to the midpoint between two policy options. Only on two occasions, February 2022 and Jane 2024, does the model predict a policy change that did not happen.

Overall, this extraordinarily simple model seems to do a reasonable job in predicting interest rate changes by the Riksbank, at least in this sample. Whether it does so out-of-sample is something that we will explore in the months to come.

I would be happy to receive comments and suggestions.