The Riksbank, SNB, Norges Bank and BoE Meetings

Punchline: The Riksbank, Swiss National Bank and Norges Bank responded to easing inflation and rising uncertainty by cutting interest rates. The Bank of England held steady, reflecting greater concern about persistent inflation and limited slack in the UK economy.

The Riksbank, Swiss National Bank, Norges Bank and Bank of England all held policy meetings on 18–19 June. While all are experiencing easing inflation and global uncertainty, their responses varied in direction and emphasis. The decisions reveal both common themes and significant divergences.

As I have argued earlier, economic conditions are often closely correlated across countries, causing central banks to adjust policy rates in broadly similar ways. As global economic conditions change, one or two central banks may change rates first and others follow after some time. While most commentary focuses on individual decisions, comparing central bank actions side by side provides useful insights into the global policy cycle and the extent to which national decisions are shaped by common forces.

Here I briefly summarise the press releases of the four central banks and compare and contrast them.

Source: Riksbank, SCB

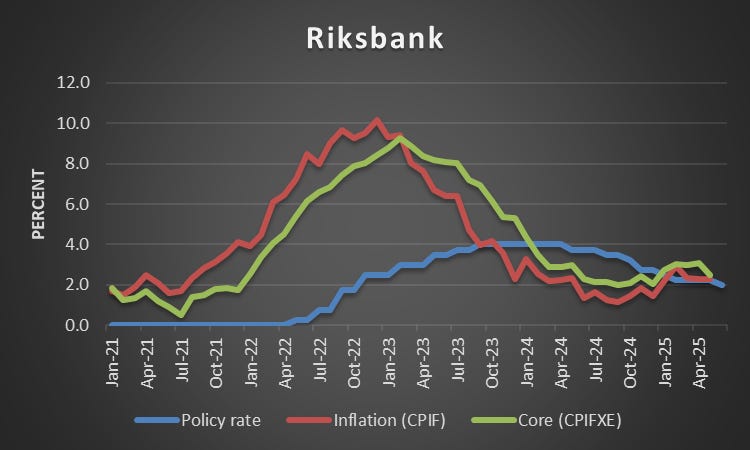

Riksbank

As expected, the Riksbank cut its policy rate by 0.25% to 2%, citing weaker-than-expected growth and a subdued inflation outlook. It noted that the recovery had lost momentum and unemployment remained high. Inflation had declined as expected and was projected to fall further due to soft demand. The rate cut aimed to support activity while keeping inflation close to target.

Geopolitical tensions and trade policy developments, including the conflict in the Middle East, were identified as key risks to global growth. Although financial markets had stabilised and tariffs were expected to be lower than initially announced in April, the Riksbank emphasised that the economic outlook remained highly uncertain. Its forecast included the possibility of another rate cut later this year, depending on how inflation and activity evolve.

Source: BfS and SNB

Swiss National Bank

The SNB lowered its policy rate by 0.25% to 0% as predicted by market pricing. The Bank noted that inflation had turned negative in May, justifying a cut to preserve price stability over the medium term. Its new forecast projected average inflation at 0.2% in 2025, 0.5% in 2026, and 0.7% in 2027, all within the Bank’s target range.

The SNB also judged that the global outlook had deteriorated since its March meeting due to rising trade tensions. Swiss GDP growth was strong in the first quarter of 2025, largely due to front-loaded exports to the US ahead of expected trade disruptions. Growth was expected to weaken again and remain subdued over the rest of the year. Overall, the outlook remained highly uncertain, with external developments posing the greatest risk.

Source: Norges Bank

Norges Bank

In an unanticipated move, Norges Bank reduced its policy rate from 4.5% to 4.25%, initiating the easing cycle much later than most other central banks, which began cutting rates in 2024. Inflation had fallen since the March monetary policy meeting and the inflation outlook for the coming year pointed to weaker inflation than predicted previously. At the same time, economic activity was assessed to be close to potential, and unemployment had risen only slightly from low levels.

The Bank described its move as a cautious normalisation rather than outright easing. While inflation was falling, it remained elevated, and there was concern that cost pressures could persist. Accordingly, the Bank signalled a gradual and careful approach to policy relaxation, noting that uncertainty around the outlook remained unusually high.

Source: ONS, Bank of England

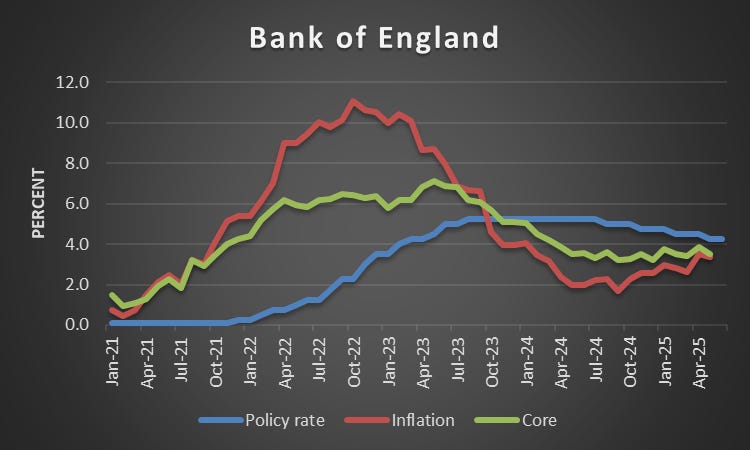

Bank of England

The Bank of England’s Monetary Policy Committee decided to keep Bank Rate at 4.25% as market participants had predicted. Three members dissented, preferring to cut rates by 0.25% to 4%. The Bank noted that inflation had declined substantially over the past two years, as earlier external shocks faded and tighter monetary policy helped anchor expectations. But a continued restrictive policy stance was necessary to contain inflation risks.

GDP growth remained weak and labour market conditions had loosened, with wage growth moderating. Inflation had increased sharply from March to April due to increases in regulated prices and earlier increases in energy prices. It was expected to stay elevated through year-end before falling in 2026. The Committee refrained from signalling the outlook for interest rates, emphasising that the appropriate policy stance would be reassessed at each meeting.

Comparing the Decisions

These central banks faced broadly similar situations. All responded to easing inflation and elevated uncertainty, with three—Riksbank, SNB, and Norges Bank—lowering interest rates by 0.25%. Each cited declining inflation as the primary reason for the move and signalled a shift toward a less restrictive policy stance. All also highlighted ongoing global risks, particularly trade tensions and geopolitical instability in the Middle East. Notably, each emphasised a data-dependent approach to future policy decisions.

There were also important differences. The SNB and Riksbank framed their decisions largely in terms of weaker inflation and subdued domestic demand and focused on keeping inflation within target and supporting a sluggish recovery, respectively. Norges Bank, by contrast, presented its decision as a cautious start to easing, despite still-elevated inflation, motivating it by a desire to avoid an excessive weakening the real economy.

In contrast, the Bank of England left Bank rate unchanged. It was more concerned about the risk of persistent inflation than the others, citing only modest labour market slack and inflation pressures as reasons to keep policy restrictive.

While inflation is low or expected to decline in all four economies, the outlook for growth remains highly uncertain. Much will depend on how global trade tensions unfold, particularly given the exceptional uncertainty surrounding US tariffs and the ongoing conflict in the Middle East. For now, central banks are adjusting their stances cautiously while keeping their options open.