Revisiting the reaction function for the SNB

Last July, I published a post entitled Interest rate setting by the SNB 2022-24. In it, I discussed a simple reaction function for the SNB that I estimated to better understand its interest rate decisions in 2022-2024. I included data from 2021, covering the period before its first interest rate increase in June 2022, since that presumably would explain why it started to raise rates. I was particularly keen to learn about what measure of inflation the SNB responded to. I also hoped to obtain an estimate of the (implied) neutral real interest, r*, in Switzerland.

The results were clear: the SNB responded to deviations of the real interest rate from r* and distributed interest changes over time, as indicated by the lagged interest rate change being significant. Furthermore, I could not reject the hypothesis of r* = -1.

Furthermore, and while I did not report it in the piece, I found no evidence that the SNB had worried about economic activity in the estimation period. That was not surprising – the key issue for it in the estimation period was plainly to stop the surge of inflation.

Given that the SNB adjusts rates quarterly, the data set comprised 14 observations over the period 2021Q1 to 2024Q2. That is far too short of a sample to say much. But the sample would grow over time, and I planned to revisit the reaction function later. I have since used that model, and a different model, in a number of posts to consider the future direction of SNB policy.

In this post I will:

review what the model predicted for interest rate changes in 2024Q3-4,

compute a forecast for 2025Q1, and

provide a direct estimate of r*.

Before proceeding, I emphasize that this analysis complements rather than replaces a careful non-technical assessment of the outlook for SNB’s interest rate decisions. This is especially important given the small sample, which necessitates a very simple specification.

The model

It is useful to be explicit about the model. Let i, π and v denote the SNB’s policy rate, the rate of inflation and a regression residual, Δ denote a change in a variable from one month to the next and let t index months (the SNB knows last month’s inflation when it sets interest rates, and the interest rate is set every three months). The model I estimated was:1

Δit = α + βΔit-3 + γπt-1 + λit-3 + vt

The estimates showed that -λ ≈ γ > 0. Rewriting the equation with that restriction imposed, we have:

Δit = α + βΔit-3 - γ(it-3 - πt-1) + vt

This indicates that the SNB adjusted interest rates in response to the real interest rate. Specifically, if the real interest rate it-3 - πt-1 was too low, the SNB raised interest rates, and if it was too high, it lowered them. The estimate of γ is approximately 0.15, suggesting that the SNB adjusted the nominal interest rate by about 1/6 at the next meeting in response to a deviation of the real interest rate from r*.

The model also indicates that the SNB adjusts interest rates gradually. The estimate of β is approximately 0.5, meaning that if the SNB raises or lowers rates by 25 bps at one meeting, it is likely to adjust them by 12.5 bps in the same direction at the next meeting. As a result, rate hikes tend to be followed by further increases, and cuts by further reductions.

Finally, note that while the SNB changes interest rates in steps of 25 bps, the model does not introduce this restriction. However, I can use the point forecast and its standard error to compute the probability distribution of the policy change. That allows me to compute the probability of different rate adjustments, as shown below.

Predictions for 2024Q3 – Q4

Next, I used the model, estimated on data through 2024Q2 with r* constrained to -1%, to generate out-of-sample forecasts for the SNB’s interest rate decisions in 2024Q3–Q4. For the September meeting, at which the SNB cut rates by 25 basis points, the model predicted a 29 basis point cut—closely aligning with the actual decision.

In contrast, the model forecasted a 30 basis point cut in December, whereas the SNB opted for a 50 basis point reduction. Two factors could explain this forecast error.

Source: my estimates

While central banks set interest rates based on expected future economic conditions, the model is entirely backward-looking, relying only on past inflation and interest rates. Although near-term inflation is often closely correlated with recent inflation, this assumption breaks down if the economic outlook shifts.

Additionally, while economic developments in Switzerland are heavily influenced by conditions in the euro area, the model considers only domestic variables. The decline in inflation and the weakening of economic conditions in the euro area at the end of 2024 may have led the SNB to conclude that also the Swiss economic outlook warranted a large cut in interest rates.

I plan to explore these issues in a future post.

Prediction for 2025Q1

What do these models predict the SNB will decide at its March meeting? Without doing any calculations, the parameter estimates discussed above are informative.

Since the policy rate is 0.5% and the inflation rate was 0.4% in January, the real interest rate is about 0% and thus above the neutral interest rate. As noted above, this suggests that the SNB would like to cut interest rates by about 15 bps.

Furthermore, since a change in one meeting is likely to be followed by half as large a cut at the next meeting, the 50 bps interest rate cut in December leads to an expected cut by 25 bps in March.

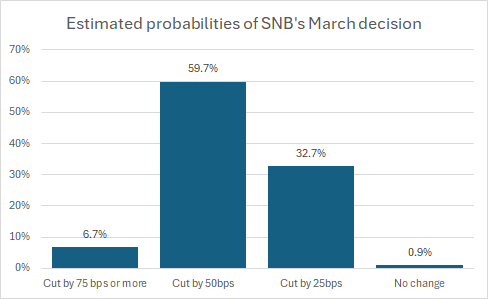

Thus, I expect a rate cut of approximately 40 bps. Formally, the model with r* = -1% yields a point forecast of a 43 bps cut with a standard error of 13 basis points.

To estimate the probability of different rate cuts, I calculate how much of the probability distribution falls within specific ranges. The probability of a 25 basis point cut corresponds to the portion of the distribution between -12.5 and -37.5 basis points, while the probability of a 50 basis point cut is determined by the range from -37.5 to -62.5 basis points, and so on. This calculation suggests a roughly 60% probability of a 50 basis point cut and a 30% probability of a 25 basis point cut.

Source: my estimates

There is still some time to go before SNB’s next policy meeting, but my sense is that a 25 bps cut is more likely than predicted by the model. The reason is that the decline in inflation outside of Switzerland seems to have stopped, and the ECB is now expected to be slower to cut rates than market commentators assumed at the end of 2024. Both considerations may impact on SNB policy. We will see what the future holds.

Estimating r*

Finally, I estimate r* directly. Note that in the steady state, Δit = βΔit-3 = vt = 0. Thus r* = α/γ. To provide a direct estimate of r*, introduce the notation μ = r* = α/γ. The model can then be written:

Δit = α + βΔit-3 – (α/μ)(it-3 - πt-1) + vt

I can then estimate μ using non-linear least squares. Using the sample ending in 2024Q2, I obtain an estimate of -1.01% with a standard error of 0.35%. Note that this is the average r* in this sample.

The views expressed are my own. The work presented is preliminary and may contain errors. It should not be construed as investment advice. Readers are encouraged to seek professional investment guidance.

In the earlier draft, I used the inflation rate from two months ago as a regressor since it was slightly more significant than the rate from one month ago. Here, I have used the inflation rate from one month ago instead.