Quick comment: Swiss Inflation Edges Higher in July

Punchline: The July CPI data vindicate the SNB’s decision not to cut rates aggressively in June; domestic inflation has held up. But further easing is still on the table, depending on external developments.

The Swiss CPI data for July are out. For those interested in SNB policy, they help frame the outlook for the September meeting.

To step back: in June, some commentators argued — in my view rashly — that with inflation falling and even turning negative in May, the SNB should cut rates by 50 basis points and return to negative interest rates.

The SNB did cut, but only by 25 basis points, bringing the policy rate to zero. The subsequently released annual inflation data for June showed that it had risen to 0.1 percent. That should not have surprised the SNB. Its own June forecast implied inflation would rise between May and June, as I noted at the time.

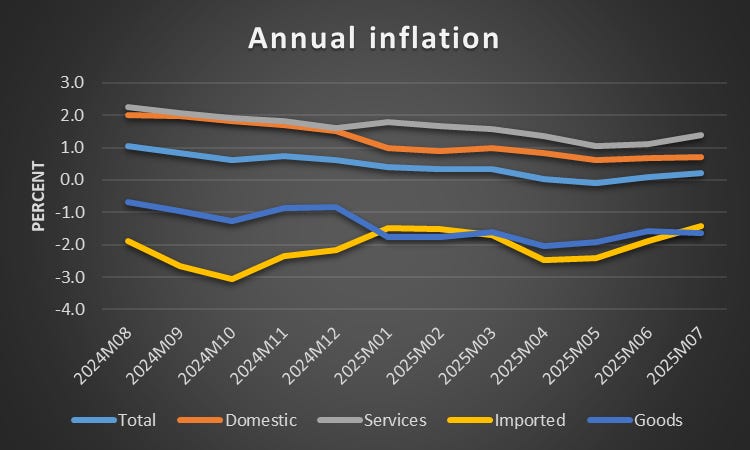

The July data strengthen the case for the SNB’s cautious move. Headline inflation rose to 0.2 percent. Domestic inflation stayed at 0.7 percent. Goods inflation remained at minus 1.6 percent. Both services and imported inflation rose. I focus on these four components because they may provide more insight into monetary conditions than the headline figure. (See for instance my earlier post here.)

Source: BFS.

Monthly Patterns and Drivers

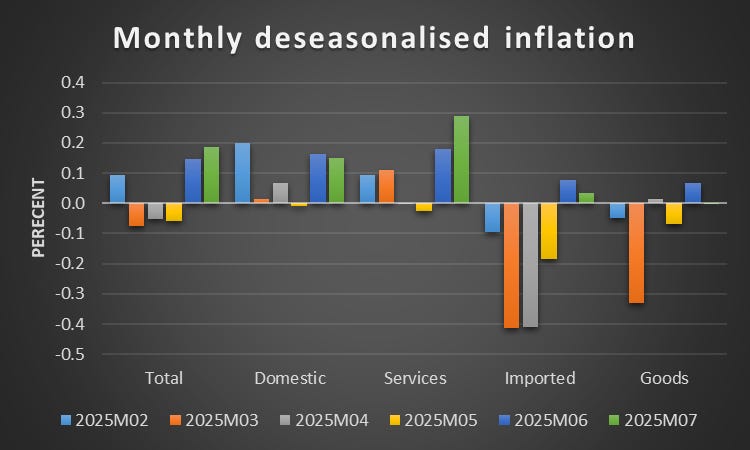

Monthly inflation developments help explain recent dynamics. The BfS does not publish seasonally adjusted data, so I have constructed my own. These should of course be interpreted with some caution.

Source: My estimates on data from BFS.

Two aspects of the second graph are of particular interest.

First, it shows that seasonally adjusted monthly inflation was 0.2 percent in July. By contrast, the unadjusted figure — which many commentators focused on — was flat. This highlights the importance of accounting for seasonal variation when interpreting short-term inflation data.

Second, the recent period of disinflation was driven by falling import prices, which declined each month from February to May. Since then, they have started to rise again, easing the downward pressure on overall inflation.

What stands out, however, is the stability of domestic and services prices during this episode. Despite the sharp drop in import prices, they barely moved, declining only slightly in May. This resilience suggests that these components reflect underlying inflationary pressures more reliably than headline or imported inflation. It is one reason why the SNB should give them particular weight when setting policy.

Outlook and Policy Implications

Looking ahead, the recent uptick in headline inflation offers some reassurance to the SNB. However, inflation remains close to the lower end of its 0 to 2 percent price stability range. Negative interest rates therefore remain a possibility, though the bar for reintroducing them is clearly high.

Much will depend on the evolving trade relationship with the United States. If the proposed 39 percent tariff on Swiss exports is implemented and remains in place for an extended period, the risk of slower growth will rise — though perhaps not as sharply as some fear. A slowdown in growth would likely reduce domestic and services inflation and put pressure on the SNB to ease policy further.

For now, the SNB retains an easing bias. Whether that bias translates into further rate cuts remains to be seen.

The SNB’s slow-and-steady approach feels pretty justified in light of July’s data. Domestic inflation staying firm while import prices do their rollercoaster routine makes a strong case for restraint. How do you think the SNB will respond if US tariffs hit Swiss exporters harder than expected?