After the June CPI Report, the SNB Looks Good

Punchline: June’s CPI data shows that the weakness of headline inflation masks more resilient domestic price trends. The SNB’s cautious stance in cutting rates to zero and refraining from going negative was well judged.

The June SNB Decision

With annual CPI inflation in Switzerland rebounding from –0.1% in May to 0.1% in June, the SNB’s decision not to reintroduce negative interest rates in June looks appropriate. The SNB almost certainly expected inflation to rebound. This was likely a key factor in its decision to refrain from a larger 0.50% cut, opting instead for a smaller 0.25% reduction that left the policy rate at 0%. A second important factor was the increased reluctance to use negative interest rates under President Schlegel.

How do we know the SNB expected inflation to rebound? In its June Monetary Assessment, the SNB forecast average inflation of 0.0% for Q2 2025. At that time, it knew April inflation was 0.0% and May inflation was –0.1%. This implies the SNB expected June inflation to be around 0.1 percent, producing a quarterly average close to 0.0%. More realistically, the SNB likely expected June inflation to fall within the range of –0.05% to 0.25%, implying a quarterly average between –0.05 and 0.05%.

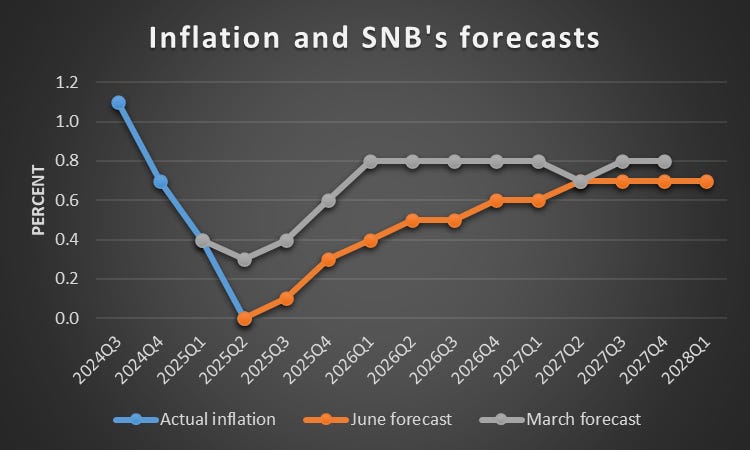

What does the SNB expect going forward? Its inflation forecast, shown below, is for inflation to remain subdued in Q3 2025 before recovering by 2027 to just under 1%, which is the midpoint of the SNB’s 0–2% price stability target. This projection is similar to the March forecast, which also expected inflation to remain weak in the near term before gradually recovering.

Source: SNB

Overall, the SNB appears to believe that the recent decline in inflation was due to temporary factors. Since inflation is calculated as the change in the price level over a 12-month period, a negative shock depresses inflation for a year before dropping out of the calculation. This matches with the SNB’s March forecast, which anticipated inflation would recover and stabilize after four quarters.

The June forecast extends this adjustment period to as long as eight quarters. It suggests the SNB expects that while past price-level shocks will gradually drop out of the calculations, new shocks will delay the recovery of inflation until 2027.

The above analysis raises three questions. First, is the SNB now “done” cutting interest rates? The answer is clearly no. New shocks and economic disturbances arise constantly, requiring central banks to respond. In that sense, central banks are never “done.”

Second, what will the SNB do as inflation approaches 0.7%? Since the SNB’s inflation forecasts are conditional on unchanged interest rates, the SNB does not expect to change interest rates.

Third, what does this imply about the natural real interest rate, r*? With nominal policy rates at zero and inflation projected to stabilise around 0.7%, the implied real rate is –0.7%. That is broadly compatible with my earlier estimate of a real rate at around –1%.

The June CPI Release

Returning to the inflation release, what is interesting are not the raw data as such, but what they reveal about the underlying dynamics of the economy. In my view, some measures are more informative about inflation pressures than others, even though all contain useful information.

The chart below presents inflation rates for goods and imports, which I consider less informative. In June imported inflation was –1.9% and goods inflation was –1.6%. Goods production is not highly labour intensive and imports, of course, are not produced at home (although import competing goods of course are). Falling goods and import prices may therefore not be problematic for the Swiss economy and do not warrant a more expansionary monetary policy.

Source: BfS

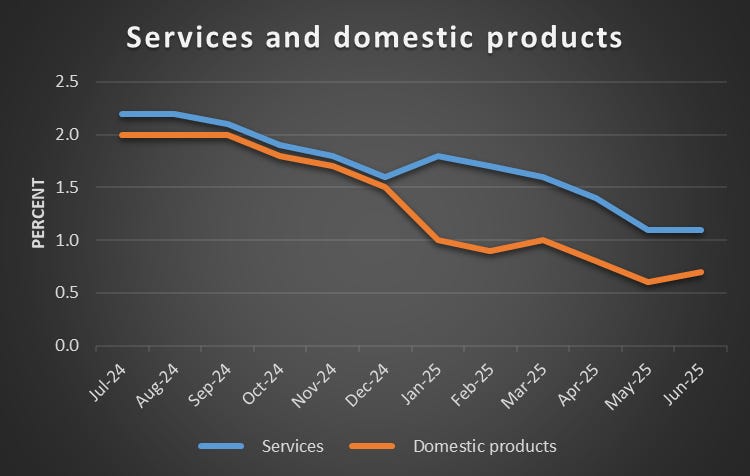

By contrast, the next chart shows inflation rates for services and domestically produced goods. Domestic inflation was 0.7% in June and services inflation 1.1%. Services are labour intensive, and domestic goods production also relies heavily on local inputs and employment. These sectors therefore provide a more direct indication of the state of the Swiss economy. Moreover, these components of inflation are quite sluggish and may therefore provide useful information about future price pressures. In June, inflation in these categories hovered around 1%.

Source: BfS

Domestic and services inflation

The SNB is surely correct in having an objective for overall inflation since it captures inflation as experienced by the public. But since goods and imported inflation are often disturbed by external developments of arguably little significant for the Swiss economy, in thinking about monetary policy it could attach greater weight to domestic and services inflation. If so, how should it interpret the current inflation rates for these components? Do they suggest that more stimulus is needed?

This is a difficult question. Some insight can be gained by looking at the historical relationship between headline inflation and domestic goods and services inflation.

Using data since January 2000, the chart below suggests that when headline inflation is 0%, domestic and services inflation have averaged just above 0.5% — somewhat below current levels. At this headline rate, imported and goods inflation have averaged around -1% or slightly lower.

Furthermore, with a headline inflation rate of 1%, all four sectoral inflation rates have averaged about 1%. This is somewhat surprising, since one might expect slower productivity growth in services to result in a rising relative price of services.

Finally, when headline inflation is 2%, domestic and services inflation have averaged just under 1.5%, while goods and imported inflation have averaged 3% or more.

There are two broad conclusions to be drawn from this sectoral analysis. First, a 0% - 2% objective for headline inflation appears broadly compatible with a 0.5% - 1.5% range for domestic and services inflation. Second, current rates of domestic and services inflation suggest that price pressures are somewhat subdued, but not as weak as headline inflation implies.

Source: My calculations

Conclusions

Overall, since inflation has fallen because of large external shocks that may have less significance than believed for the Swiss economy, it makes sense to place some weight on domestic and services inflation rather than focusing solely on the headline rate when judging policy. On that basis, some monetary stimulus appears warranted. But unless new shocks emerge, a prolonged period of deflation in Switzerland remains unlikely. In my view, cutting interest rates to 0% was appropriate and will help support a gradual firming of inflation.

This is rather compelling - I especially appreciate the nuanced focus on domestic vs headline inflation. It's easy to overreact to headline figures, but your analysis reminds me how misleading they can be in isolation. According to a BIS study, central banks that rely too heavily on volatile headline data risk policy lag and misfires (bis.org).

Would you say the SNB’s communication strategy matches its policy precision, or is there a gap?