Quick comment: Are market expectations pushing the Fed towards a 50 bps cut?

2024-23

In recent days there have been large fluctuations in the probability that market participants attach to the Fed cutting interest rates by 0.25% or 0.50% at its meeting this week. Market participants seem increasingly to be of the view that the Fed will cut interest rates by 50 bps. Will that push the Fed towards a 50 bps cut?

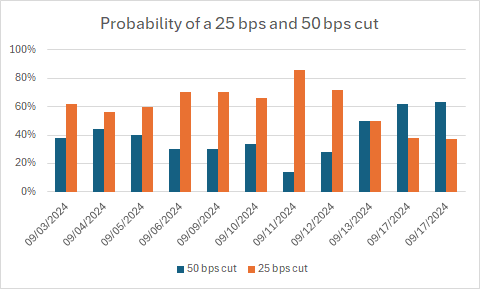

The graph below shows what the market has been pricing in, as calculated by the CME Fed Watch calculator. Just a week ago, markets were pricing in a 25 bps cut with 2/3 probability and a 50 bps cut with 1/3 probability. However, five days ago the markets saw both outcomes as equally likely, and by yesterday the situation had been reversed. These are large changes in a very short period.

Source: CME

Some commentators think this is a one-sided game in which shifting expectations have no impact on what the Fed will do. The argument is that central banks should just set the interest rate they think is appropriate. What the market thinks is, in their view, irrelevant.

That extreme position, which is held by few central banks (except possibly by the SNB), is odd. In practice, a central bank seeks to balance two considerations.

First, it would like to set the interest rate, r, as close as possible to the macroeconomically warranted interest rate, rM. The latter appears to have dropped like a stone in recent weeks as there have been growing signs that the US labour market is cooling, and inflation pressures are abating.

Second, it wants to avoid surprising financial markets. There is always a risk that some financial institutions are poorly positioned and that a large interest rate change could lead them to experience potentially catastrophic losses. That could lead to a burst of financial tensions and instability which the Fed is keen to avoid. To do so, they want to set the interest rate not too far away from the interest rate expected by financial institutions, Er. This is why arguments such as “the Fed should just go big” cuts no ice with FOMC members.

We can think of this as the Fed wanting to minimise the squared deviation of r from rM and of r from Er: (r – rM)2 + k(r – Er)2, where k denotes the relative importance attached to not surprising markets. Most central banks, including the Fed, act as if k > 0.

The solution to this minimisation problem is to set r = (rM + kEr)/(1 + k).

To see what this means, suppose that the Fed does not care what the market expects it to do, that is, k = 0. In that case the Fed will set r = rM, that is, it will set whatever interest rate it thinks is appropriate from a macroeconomic perspective.

Next, suppose that the Fed only cares about financial stability, that is, k → ∞. In that case the Fed will set r = Er, that is, it will deliver whatever interest rate the market expects in the hope of avoiding surprising financial institutions.

Finally, suppose that the Fed attaches equal weigh on the two objectives, that is, k = 1. In that case it will set r = (rM + Er)/2, that is, the Fed will set r equal to the average of interest rate warranted on macroeconomic grounds and the interest rate expected by the market.

Thus, if k > 0, the Fed worries – a lot or a little – about surprising financial institutions, then what markets expect matter for the Fed’s decision. The lower Er is, the more the Fed will cut the interest rate. The fact that expectations have taken hold that the Fed will go for a large cut has thus made that outcome more likely.

This is why central banks try to communicate clearly and manage expectations about the future path of policy. Indeed, these shifting expectations reflect how markets perceive the Fed’s response to incoming data. If the Fed has clearly communicated its reaction function, then this shift in expectations is exactly what the Fed would want: they can cut rates sharply in response to new data without fear of causing any financial instability.

This makes the process sound very cooperative. Can the probabilities be manipulated by markets to get the Fed to do something it wants? That seems unlikely. While, for instance, the LIBOR scandal showed that participants could manipulate the rate for their own gain, LIBOR was determined by a relatively small set of market participants and was essential a survey of opinions. That is quite different from the market data that the CME’s calculations are based on.

In sum, I am guessing that market expectations will have pushed the Fed into a 50 bps cut. We will know for sure later today.

Very interesting conclusion that the market will push the Fed to do 50bp today, and very elegant way of deriving it. I strongly recommend reading it.

I'm not sure I agree with the line of argument however - on normative grounds. If the central bank in every decision makes sure it doesn't disappoint the market - a kind of central bank put writ large - then this stores up trouble for the future as it creates moral hazard: the financial sector will take bigger and bigger risks knowing the central bank will not want to upset the apple cart.

** Nerds only: in the model, the result is due to the one shot nature of the game in a Barro-Gordon-type setup; in fact it should lead to a suboptimal equilibrium like the inflation bias in BG (1983), where you get too much market volatility as the central bank can't commit [Stefan please correct me if I'm wrong as I'm rusty on all this grad school macro] **

If this is how the central bank behaves, the end result is financial dominance: the central bank must deliver whatever the market, or the financial sector, needs.

A related problem is that of communication: I'm of the view that central banks shouldn't issue guidance but in exceptional cases (e.g. lower bound), see here: https://open.substack.com/pub/thinicemacroeconomics/p/the-ecb-should-resist-the-forward?r=1oa8fn&utm_campaign=post&utm_medium=web

Jeremy Stein has a great paper on this whole conundrum which I link to in my post.

Thank you for the stimulating read Stefan Gerlach.