How worried should the SNB be by 0.6% inflation?

2024-37

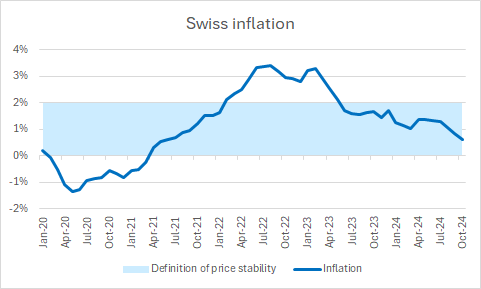

At the SNB and its Watchers 2024 conference last week, SNB Chairman Martin Schlegel discussed its monetary policy framework. He emphasised that the framework needed to allow for flexibility in terms of inflation, given the exceptional openness of the economy and the fact that external shocks often have a major impact on Swiss prices. This is why the SNB defines price stability as any inflation rate between 0% and 2%.

Source: BfS and SNB

He went on to say that the October inflation rate of 0.6% rate is well within the SNB’s 0-2% price stability range and signalled that while the SNB is not a fan of negative interest rates, it would not hesitate to reintroduce them if that became necessary to achieve and maintain price stability.

How worrying is the low Swiss inflation rate?

While Chairman Schlegel did not seem concerned by the low inflation rate, before the SNB’s September meeting many commentators, me included, speculated that the SNB could cut interest rates by 0.5% because of the inflation outlook. Some even expected it to do so. The most recent CPI release available at that time (which was for August) showed inflation at 1.1%.

In the end the SNB cut interest rates by 0.25% but lowered its inflation forecasts materially. For 2024Q4 it lowered its projected inflation rate from 1.4% in June to 1.0%. It forecast inflation to continue to fall to 0.5% in 2025Q2-Q4 before rebounding. It also stated that:

Further cuts in the SNB policy rate may become necessary in the coming quarters to ensure price stability over the medium term.

Since then, inflation has fallen further to 0.8% in September and 0.6% in October. With electricity prices scheduled to fall substantially in January, the September forecasts appear optimistic. Given that inflation fell 0.5% between August and October, it seems quite possible that inflation could fall to zero or even below zero in the next few months.

Some calculations

How likely is it that inflation will fall below zero? Or rise above 2%? One way to assess these probabilities is to estimate a simple time series model for inflation and compute forecasts and associated confidence bands. While the SNB surely uses more elaborate models, simple time series models do a surprisingly good job forecasting many macroeconomic time series in the short term. You can sometimes do better with a more elaborate model, but not by much.

So I estimated an ARMA(2,12) model for annual inflation using monthly data spanning 2000 – October 2024, produced forecasts and associated standard errors for the period until the end of 2025, and used these to compute the probability that inflation would be below 0%, between 0% and 2%, and above 2% at the time of the next five SNB meetings. The graph below shows the results.

Source: my calculations on data from BfS.

They can be expressed very simply. The risk that inflation will be below 0% at the December 2024 SNB meeting is about 8% (or 1/12); it is 16% (or 1/6) in March, 24% (or 1/4) in June 2025 and 18-20% (or 1/5) in September and December 2025. According to the model there is a significant probability of inflation undershooting the target range. In hindsight, the decision to cut by merely 0.25% in September seems a little complacent.

The probabilities of inflation increasing above 2% were calculated to be 0% in December 2024 and rise to 10% in December 2025.

Are these results surprising? For comparison, in 27% or almost 1/3 of the 298 observations in the sample used to estimate the model, inflation was negative. In 9% it was above 2%. By that standard, these numbers are plausible.

Conclusions

With a 0-2% inflation objective and a policy rate of 1%, facing a 1/4 risk of being in deflation by June must make the SNB a little uncomfortable.

It is sometimes argued that with interest rates close to zero, central banks should “keep the gun powder dry” and become increasingly hesitant to cut rates further as they approach zero.

That intuition is nonsense. The formal economics literature argues the opposite: the central bank should take prompt action to avoid amplifying the low inflation problem. If the SNB wants to avoid having to lower interest rates to zero or below, it should cut interest rates aggressively at its next opportunity. That may prevent inflation from falling too low, requiring it to adopt negative interest rates again.