The Governing Council’s October decision: What I learned as a former fly-on-the-wall

2024-30

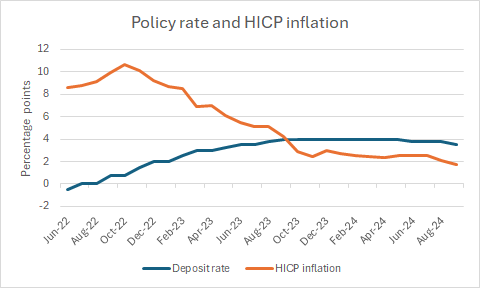

Source: ECB

The ECB cut interest rates for the third time in four months by 0.25% to 3.25% at its meeting on 17 October. The ECB’s deposit rate has now been lowered from 4% to 3.25%. That is cumulatively a significant move.

Source: ECB

While this cut was expected by market commentators, at the time of the September meeting, President Lagarde gave no indication that the Governing Council was on a path to cut interest rates in October. Rather, she emphasised that the Governing Council “shall be data-dependent. We shall decide meeting by meeting. And our path, of which the direction is pretty obviously a declining path, is not predetermined neither in terms of sequence nor in terms of volume.”

Governing Council decision making

So, the Governing Council cut interest rates because the data told it to do so, not because it was executing a previously formed plan to lower rates. But which data? To get a handle on this, it is useful to make a detour into ECB decision making. The thoughts below reflect some views about Governing Council decision making that I formed while attending as an Irish “back seater” in 2011-15.

There is no single view that determines policy. With 26 members of the Governing Council – the six members of the Executive Board and the 20 National Central Bank governors – policy is an outcome of a constellation of views.

In my experience, complex explanations according to which the Governing Council cut or raised interest rates because members weighted and ranked in terms of their importance several considerations are often wrong.

Indeed, since policy is set in a half-day meeting (although different Governing Council members may of course speak in advance), there is simply too little time for such a time-consuming exercise. If the meeting starts at 9 am, the introductory reviews of current economic and financial conditions made by Philip Lane and Isabel Schnabel take 45 minutes each, and the remaining 24 members speak for five minutes each, then it is 12:30 pm before the tour-de-table is completed. With a statement to be agreed in time for the 14:15 press release and perhaps a range of related minor decisions to be taken, there is too little time for a thorough discussion.

Policy is changed because most members feel a compelling case has been made for an interest rate cut or increase. However, they may have quite different explanations for why it was warranted.

Take the current situation. Many commentators have argued that a stream of data suggesting weak economic activity was a key factor underpinning the decision. It may have been. To be sure, some members will have worried about slower growth and the risk of a full-blown recession and will have argued favour of lower rates to support the real economy.

But others will have been hesitant. During the years I attended influential members often argued that too little is known about the current state of the real economy to respond vigorously to it. While it may look like it is slowing precipitously or picking up rapidly, revised data may tell a very different story in six- or nine-months’ time.

Furthermore, they argued, since it takes a long for the economy to respond to policy changes, there is a risk that the economy will already have returned to trend growth by the time policy comes online. Reacting to the perceived state of the economy therefore runs the risk of amplifying economic fluctuations. These arguments were compelling to many members of the Governing Council.

Facts matter more that forecasts. Arguments for changing policy are often based on a forecast that otherwise something bad will happen. But Governing Council members know from experience that forecasts are often wrong and that the public is dubious about economists’ ability to predict the future. Justifying to the public a decision that ended up being misguided with the argument that it was based on a forecast may not seem like a winner to them. NCB governors are keen to guard their reputation and therefore shy away from making decisions that may be difficult to sell to a sceptical public. Relying on facts is better.

The ECB’s mandate is critical. Decisions that are directly tied to the mandate are the easiest to build consensus behind. The ECB does not have a mandate for growth, but it does have a mandate for 2% HICP inflation.

The October decision

What does that mean for the October decision? In my view, by far the most important factor underpinning the decision was the fall in headline inflation in the euro area to 1.7% in September from 2.2% in August. It is a large move in the single variable for which the ECB has an objective. And it is a fact, not a debatable forecast.

Of course, some participants worried about growth, but others probably did not. Some will have worried about the Fed cutting interest rates aggressive in the coming months, leading the euro to strengthen and inflation to fall further unless the ECB cut rates too. Whatever their precise reasons, they were all in favour of a cut.

A auxiliary factor that will have played a role is the knowledge that the strength of an interest rate change grows over time as financial contracts expire and new contracts are entered into. Sure, some households may delay a decision to move and enter a new mortgage contract, and some firms may delay bank lending, but they cannot do so permanently. With the effects of policy growing stronger and with inflation softening, the mood music must have been in favour of an interest rate cut.

In passing, it is interesting to note what explanations the decision to cut rates is not compatible with. It is difficult to reconcile it with the view that the ECB is focusing on services inflation and wage growth, both of which are continuing to run high. And it is not compatible with the idea that the ECB targets stock prices, which are rising.

My model forecast

I have been using a series of embarrassingly simple single-equation models to analyse interest-rate setting by the SNB, the Riksbank and the ECB. Again, these models are not intended to substitute for a careful analysis of economic conditions, but rather to serve as a benchmark for such an analysis. If the model predicts a different outcome from the conclusion the rest of the analysis leads to, then it is time to reconcile the two views.

In my earlier piece on the October decision, I calculated the probability that the Governing Council would cut interest rates by 0.25% or leave them unchanged, as a function of HICP inflation September. While I did not know what that inflation rate would be, I expected it to below the 2.2% recorded in August and at which the probabilities of a cut or interest rates being left unchanged appear balanced.

Let me present the information in that graph somewhat differently:

Source: my estimates

I noted in my piece that if inflation fell as low as 1.8%, the probability of a 0.25% cut would be 78%. In fact, September inflation was even lower, 1.7%, and the predicted probability of a 0.25% cut was even higher, 83%. The decision to cut rates was thus entirely compatible with the Governing Council’s responses to inflation since the summer of 2022.

Note that the model only includes the interest rate set by the Governing Council at the last meeting and headline inflation – it doesn’t include a variable capturing growth. Nevertheless, the model predicted a cut. It appears that the behaviour of inflation is sufficient to account for the cut.

Conclusion

As inflation fell sharply in September, the Governing Council cut interest rates. Commentators have put forward several possible reasons for this. My guess, from having been a fly on the wall during earlier Governing Council meetings, is that the growth outlook was less important than some would suggest. It seems more likely to me that the low incoming inflation data was the key driver of the decision to cut rates. My very simple model of ECB decision making, which relies only on the inflation rate, suggests that the September rate of 1.7% was low enough to prompt a rate cut.

Do you think the so called "data-driven appproach" of the ECB is something that have intensified in the post-covid era or is it something that was present before? From your writings I get the sense that the ECB decision making has always being super data driven an avoided forecast and the fact it has so many participants and so little time to make the rates decision intensifies it. On the other hand, I feel that the data-driven approach is a post-covid phenomenon and it is not related to the size of the ECB board, since the FED, BoE etc are all following this approach.