Could the SNB cut interest rates by 50 bps?

2024-22

The SNB is likely to cut interest rates several times in the coming quarters, much like the ECB and the Federal Reserve. Market pricing attaches a high probability to the FOMC cutting by 0.5% when it meets later this week. I was asked by

whether it is possible that the SNB will cut by 50 bps too? That is an interesting question that I had not thought much about. It is the focus of this post.SNB interest rates

SNB introduced interest rate targeting in 2000. The graph below shows “policy rates” for the SNB and the Federal Reserve (which is either the policy rate or target for the federal funds rate; or the midpoint of the target rate band when there is no single interest rate), and the deposit rate for the ECB since 2000. Since the SNB sets interest rates quarterly, quarterly data are used.

The lesson of the graph is that the major swings in all three interest rates coincide with easily identifiable shocks that make it obvious that monetary policy needs to be recalibrated. These central banks all cut interest rates in the early 2000s as the dot.com bubble burst and a risk of recession took hold; they cut rates as Lehman Brothers collapsed in the autumn of 2008 when the Global Financial Crisis started, and they raised rates in 2022 as post-covid inflation took hold. Plainly the SNB is more likely to cut interest rates if the ECB and the Federal Reserve do so.

Source: SNB, ECB, FRED

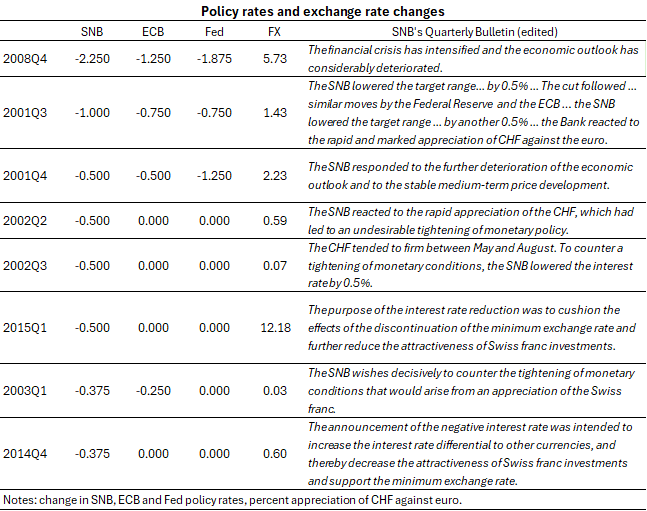

Episodes of large SNB cuts

The table below looks at the episodes in which the SNB cut interest rates by more than 25 bps and includes some (lightly edited) quotes from the SNB’s Quarterly Bulletin motivating the policy changes. The table also shows the changes in policy rates of the ECB and Federal Reserve in those quarters, together with the quarterly change in the Swiss franc against the euro.

It is clear from the table that large interest rate cuts were undertaken in periods of economic weakness, when the ECB and the Federal Reserve also cut interest rates, and in episodes of currency strength. In many cases, these changes were undertaken through a series of cuts, often outside of the regularly scheduled quarterly policy meetings.

Sources: SNB, ECB and Federal Reserve

A model

Next, I regress the change in the SNB policy rate on the changes in the ECB’s and Federal Reserve’s policy rates, and on the percentage change in the exchange rate against the euro, in the same quarter. I think of the model as purely statistical and not as a well-defined empirical reaction function. Including the exchange rate is a little dicey because an expected change in the policy rate presumably influences the exchange rate. Thus, there is an issue of simultaneity of unknown severity. I assume that it is negligible, which might be wrong. That said, in a reduced form model of this type, that might not matter.

The parameter on the changes in the ECB’s and the Federal Reserve’s policy rate are 0.51 (t = 6.5) and 0.18 (t = 3.3). The parameter on the change in the exchange rate is -0.03 (t = 3.3), implying that a one percent strengthening of the Swiss franc against the euro lowers the expected change in the SNB’s policy rate by 3 bps. The r-squared is 56%.

I then use this model to compute the predicted change in the SNB’s policy rate for 2024Q3. I assume that the change in the ECB’s policy rate is -25 bps, and that the Swiss franc appreciates by 3.2% against the euro in the quarter. If I assume that the Federal Reserve cuts rates by 25 or 50 bps, the predicted change in the SNB’s policy rate is -28 or -32 basis points, in each case with a standard error of 23 bps.

These results suggest that the SNB is very likely to cut rates by 25 bps. But they also suggest that there is some probability that will cut rates by more than so (and, of course, some small probability that it will leave them unchanged or even raise them).

Since I have the mean and standard deviation of the predicted change, I can calculate these probabilities. To do so I assume normality – that might also be wrong, but it seems like a reasonable starting point.

I calculate the probability mass for a cut of more than 67.5 bps and refer to that as the probability of a cut by 75 bps or more. Similarly, I calculate the probability of a cut of between 37.5 bps and 67.5 bps and refer to that as the probability of 50 bps cut, and so on.

The results are interesting: the probability of a 50 bps cut is about 30% and the probability of a 25 bps cut is about 40%. Overall, whether the Fed cuts by 25 or 50 bps has little impact on the estimated probabilities. (There is also about a 20% probability of no change or an increase in the SNB’s policy rate. Commentators often forget that odd things can happen and disregard the probability of such outcomes. But the SNB raised interest rates by 25 bps in 2007Q3 when the Federal Reserve cut interest rates by 50 bps and the ECB left them unchanged.) Thus, the probability of a 50 bps cut is almost as large as the probability of a 25 bps cut (!).

Source: my calculations as described in the text.

Conclusions

These back-of-the-envelope calculations are all illustrative and much could be wrong with them. Nevertheless, and to the extent that history is a guide, they suggest that the SNB could cut rates by 50 bps later this month, particularly if the Federal Reserve decides to cut them by 50 bps. While I am nevertheless guessing that it will cut rates by 25 bps, having done this exercise I recognise that a larger cut is possible.

Brilliant. So, the SNB’s rate change is principally a function of the ECB’s rate change, absent other factors. And independently of that, ‘unwarranted’ CHF strengthening can act as a driver of rate cuts, at times outside of scheduled SNB meetings. Also, it seems to imply that Fed’s 25v50bps on Wednesday is not a key driver of what SNB would do a week later. Thank you Stefan!

Very interesting analysis. It will be also interesting to see how market probabilities would change this coming Wednesday as the Fed chooses between 25 or 50bps. Basically, what is current market perception of the reaction function of the SNB to shift in the Fed fund rate (given that in one way or another there is going to be a surprise)?